All Categories

Featured

Table of Contents

[/image][=video]

[/video]

This can result in much less benefit for the insurance holder contrasted to the economic gain for the insurance provider and the agent.: The illustrations and assumptions in advertising products can be misleading, making the policy appear a lot more eye-catching than it could in fact be.: Be aware that economic advisors (or Brokers) earn high compensations on IULs, which could affect their recommendations to sell you a plan that is not appropriate or in your ideal interest.

Most account alternatives within IUL items assure among these restricting variables while enabling the other to drift. The most common account alternative in IUL plans features a floating annual rate of interest cap between 5% and 9% in existing market problems and a guaranteed 100% participation price. The rate of interest gained equals the index return if it is less than the cap yet is topped if the index return surpasses the cap rate.

Other account choices may include a drifting engagement price, such as 50%, without cap, implying the interest credited would be half the return of the equity index. A spread account credit histories interest over a floating "spread out rate." If the spread is 6%, the rate of interest credited would be 15% if the index return is 21% yet 0% if the index return is 5%.

Rate of interest is normally attributed on an "annual point-to-point" basis, suggesting the gain in the index is computed from the factor the premium went into the account to exactly one year later. All caps and engagement prices are then applied, and the resulting rate of interest is attributed to the plan. These rates are adjusted every year and utilized as the basis for computing gains for the following year.

The insurance coverage firm purchases from a financial investment financial institution the right to "buy the index" if it exceeds a certain degree, understood as the "strike price."The provider could hedge its capped index liability by acquiring a call alternative at a 0% gain strike price and composing a telephone call alternative at an 8% gain strike price.

Is Iul Insurance A Good Investment

The budget that the insurance provider needs to purchase options depends upon the yield from its basic account. If the service provider has $1,000 web costs after deductions and a 3% return from its general account, it would certainly allocate $970.87 to its basic account to expand to $1,000 by year's end, using the staying $29.13 to purchase options.

This is a high return expectation, reflecting the undervaluation of choices out there. The two largest aspects influencing drifting cap and involvement rates are the yields on the insurance provider's basic account and market volatility. Service providers' basic accounts mainly contain fixed-income possessions such as bonds and home loans. As returns on these properties have decreased, carriers have actually had smaller allocate purchasing choices, bring about minimized cap and engagement prices.

Carriers generally show future efficiency based on the historical efficiency of the index, using current, non-guaranteed cap and involvement rates as a proxy for future efficiency. This technique may not be realistic, as historical estimates commonly show higher previous rates of interest and assume consistent caps and engagement prices despite varied market problems.

A much better strategy might be alloting to an uncapped participation account or a spread account, which entail getting reasonably affordable options. These techniques, nevertheless, are less steady than capped accounts and might need frequent changes by the carrier to reflect market problems accurately. The story that IULs are conventional products providing equity-like returns is no much longer sustainable.

With reasonable expectations of options returns and a diminishing budget for buying choices, IULs might give marginally greater returns than traditional ULs but not equity index returns. Possible customers must run images at 0.5% over the rates of interest attributed to standard ULs to evaluate whether the policy is effectively funded and qualified of providing guaranteed performance.

As a relied on companion, we team up with 63 top-rated insurance companies, guaranteeing you have access to a diverse range of options. Our solutions are completely complimentary, and our professional consultants supply objective guidance to aid you locate the best insurance coverage customized to your requirements and budget. Partnering with JRC Insurance policy Group indicates you receive personalized service, competitive rates, and satisfaction recognizing your financial future is in qualified hands.

Www Iul

We assisted thousands of family members with their life insurance policy requires and we can help you too. Created by: Louis has actually been in the insurance coverage service for over 30 years. He specializes in "high danger" cases in addition to more complicated insurance coverages for long-term treatment, special needs, and estate planning. Specialist assessed by: Cliff is an accredited life insurance policy representative and one of the owners of JRC Insurance policy Group.

In his extra time he appreciates spending quality time with household, traveling, and the open airs.

For aid in recurring evaluation and surveillance this harmonizing act, we suggest you consult our associated business, Strategy Trackers, Inc.Furthermore, as long as this cash money value collateral surpasses the funding and its accrued passion, the loan never ever requires to be settled throughout the life time of the guaranteed. If, as anticipated, the collateral grows faster than the funding, the funding is paid off at the fatality of the guaranteed. Indexed global life insurance, likewise referred to as equity indexed universal life insurance policy, has all of the aspects of standard global life insurance coverage. The distinction exists in the way a section of costs down payments is spent. Component of each costs, while not directly purchased equities, will pattern any kind of credited gain after the efficiency of a certain equity index or multiple equity indices. Efficiency of these products introduces substantially more volatility.

Indexed Universal Life Insurance Calculator

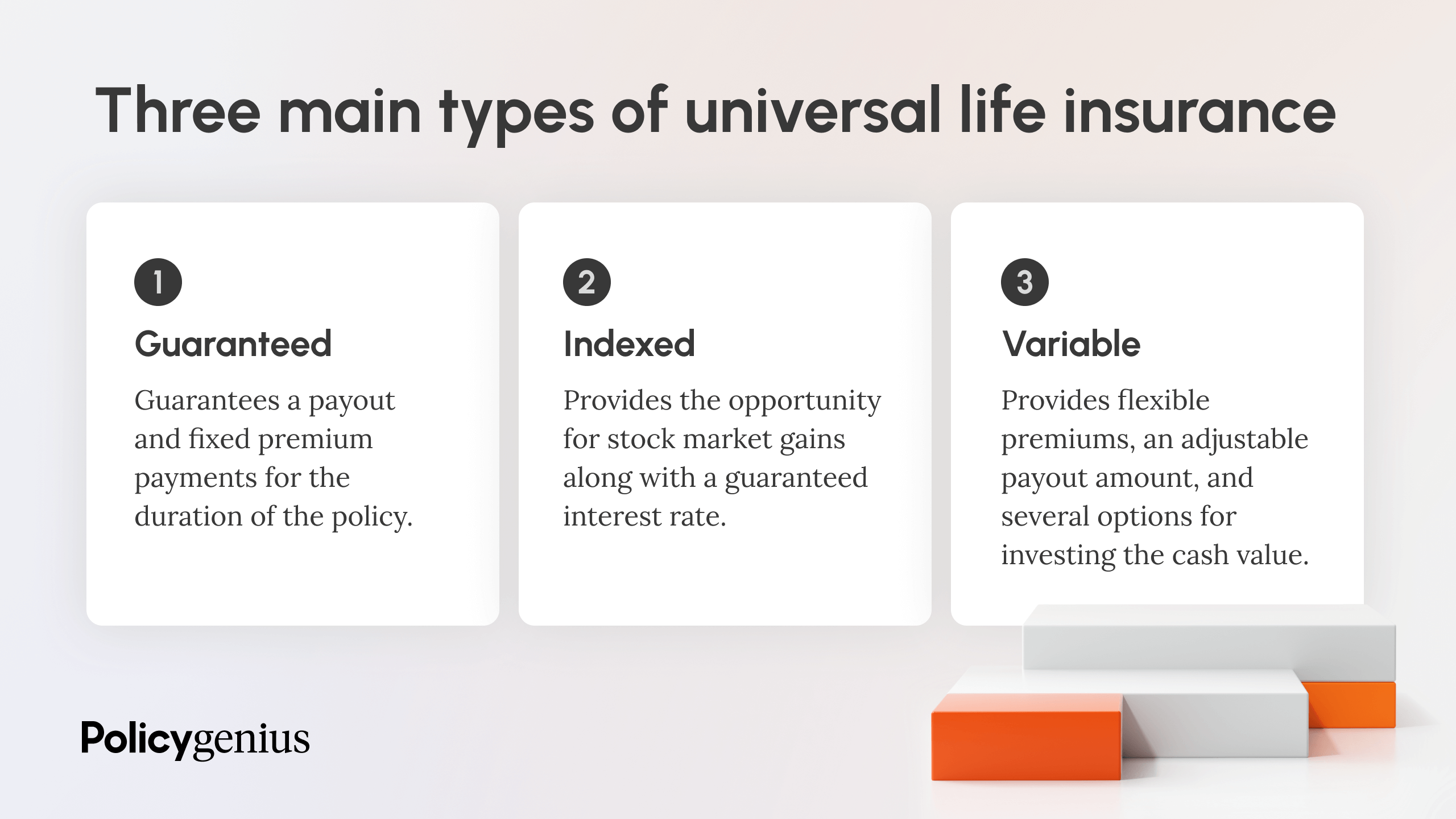

in years where there is a positive credit, that credit has credit history potential to possible more than doubled. Each container of invest-able funds imitates the performance of one or even more of these indices. Real return to the policyholder will depend not only upon the efficiency of one or even more of the provided indices, but likewise upon the cap, flooring, spread, and participation price that is in location for each provided sector (pail)created within the plan. This makes it an eye-catching option for those that desire development potential without the danger connected with standard investments.: The cash worth within an IUL plan grows tax-deferred, meaning insurance holders do not pay tax obligations on the growth. In addition, when structured correctly, IUL permits tax-free withdrawals and fundings, using a beneficial method to accessibility funds throughout retired life. This policy design is for the consumer who needs life insurance policy yet would certainly such as to have the capacity to select exactly how their cash money worth is invested. Variable policies are financed by National Life and dispersed by Equity Providers, Inc., Registered Broker/Dealer Affiliate of National Life Insurance Policy Company, One National Life Drive, Montpelier, Vermont 05604. Premiums on some items are not ensured and might raise at a later day. Be certain to ask your economic expert regarding the lasting treatment insurance plan's functions, benefits and costs, and whether the insurance coverage is proper for you based upon your financial scenario and objectives. Handicap earnings insurance usually provides regular monthly earnings advantages when you are incapable to function as a result of a disabling injury or illness, as specified in the plan. 1 Permanent life insurance policy contains two kinds: whole life and universal life. Money value expands in a participating entire life policy with dividends, which are stated every year by the firm's board of directors and are not ensured.

Cash value grows in a global life plan through credited rate of interest and lowered insurance costs. If the policy gaps, or is surrendered, any kind of outstanding loans finances taken into consideration in the policy may might subject to ordinary income earningsTax obligations A dealt with indexed universal life insurance (FIUL)plan is a life insurance product item provides supplies the opportunityChance when adequately properlyMoneyed to participate get involved the growth of the market or an index without directly investing spending the market.

{kind=link}

Latest Posts

Flexlife Indexed Universal Life

What Is Indexed Universal Life Insurance?

Iul Università